Why do not all pension funds pursue a dynamic balance sheet policy?

Dynamic balance sheet policy is rational but feels counterintuitive

Dynamic balance sheet policies reduce the risk of benefit cuts and non-indexation. However, by no means all funds pursue this rational risk policy, because it feels counterintuitive.

By Noortje de Beijer, Head of clients at Cardano

Dynamic balance sheet policy involves managing funding level risks by adjusting your policy as funding levels rise or fall, instead of waiting for the multi-year assessment to make changes. You reduce risk at low funding levels and funding levels between 130% and 150%. You increase risk when you are unable to guarantee all future indexation, i.e. between low funding levels and approx. 130%.

We tend to all or nothing

The fact that this feels irrational is largely due to our tremendous mental resistance to taking losses when things are going badly and ‘taking profits’ when things go well. Loss aversion is quick to increase everyone’s appetite for risk when losses loom on the horizon. Although this does increase the chances of recovery, it simultaneously boosts the odds that funding levels will drop even further. We tend to all or nothing. When things are going very well, we are inclined to take bigger risks, on the pretext of ‘we’re doing well, right?’ and ‘we can take it’. We become euphoric.

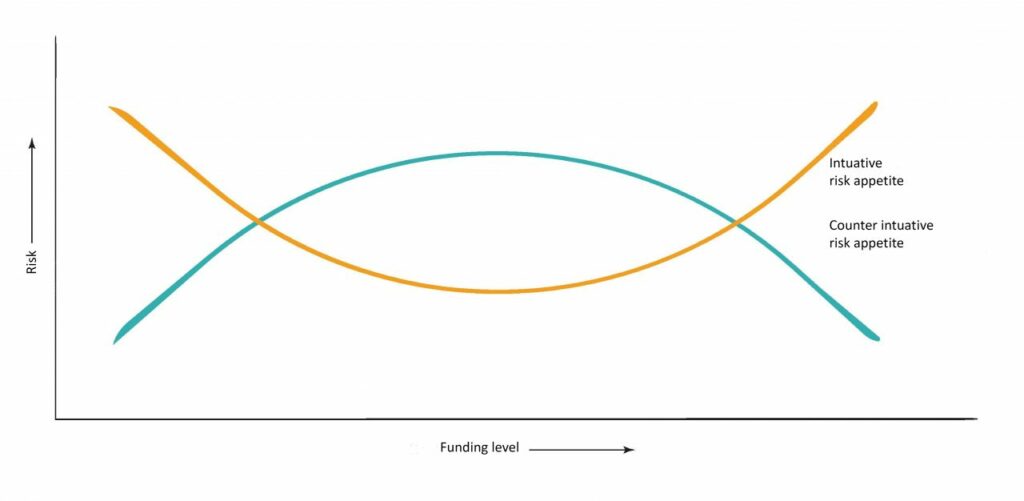

The graph below illustrates the difference between our intuitive risk appetite and our risk appetite when pursuing a dynamic balance sheet policy.

Awareness and discipline

How can executives avoid these cognitive pitfalls? It starts with awareness, followed by discipline. Define your dynamic risk policy before your fund ends up with troubling funding levels and make it default policy. By the time a particular situation does occur, you will have already thought about it and have protected yourself from excessively risky behaviour. Will it still be possible to deviate from the established risk policy, should the situation so require? Of course it will, but you will have to come up with good arguments. Either way, it will change the nature of the discussion.

Eliminating uncertainty

This is how Dynamic balance sheet policy eliminates any uncertainty about whether or not to take action and whether it is already too late. Because it aligns risk policy more closely with the fund’s pension objectives, it provides peace of mind and contributes to a more robust investment policy.